ESPCI web site

ESPCI web site

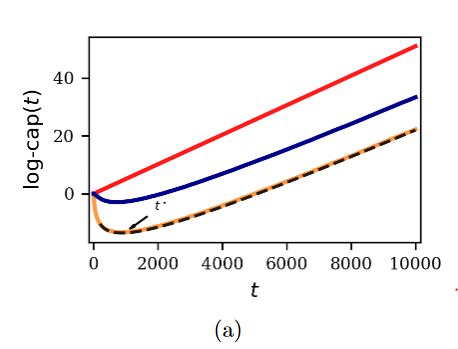

We formulate an adaptive version of Kelly’s horse model in which the gambler learns from past race results using Bayesian inference. We characterize the cost of this gambling strategy and we analyze the asymptotic scaling of the difference between the growth rate of the gambler and the optimal growth rate, known as the gambler’s regret. We also explain how this adaptive strategy relates to the universal portfolio strategy, and we build improved adaptive strategies in which the gambler exploits the information contained in the bookmaker odds distribution.

We formulate an adaptive version of Kelly’s horse model in which the gambler learns from past race results using Bayesian inference. We characterize the cost of this gambling strategy and we analyze the asymptotic scaling of the difference between the growth rate of the gambler and the optimal growth rate, known as the gambler’s regret. We also explain how this adaptive strategy relates to the universal portfolio strategy, and we build improved adaptive strategies in which the gambler exploits the information contained in the bookmaker odds distribution.

JOURNAL OF STATISTICAL MECHANICS-THEORY AND EXPERIMENT

Volume: 2022

Issue: 9

Article Number: 093405

Published: SEP 2022

By: Despons, Armand ; Peliti, Luca ; Lacoste, David